Payments on Furniture: A Central Florida Buyer’s Guide

A lot of Central Florida families run into the same moment. You've found the sofa that finally feels right, or the dining set that fits your new home in Lake Mary or Sanford, and then the practical question shows up fast. What's the smartest way to handle payments on furniture without stretching your budget too far?

That question matters more than ever because flexible payment plans have become a regular part of how people shop for home furnishings. A 2025 industry summary says the U.S. furniture market is valued at between $193 billion and $250 billion, and home goods make up up to 42% of Buy Now, Pay Later purchases (industry summary on furniture and BNPL). For real households, that means more shoppers are using payment options to furnish bedrooms, living rooms, and dining spaces in a manageable way.

If you're trying to make a thoughtful decision, it helps to slow the process down. A furniture purchase isn't just about whether a monthly number looks comfortable today. It's about total cost, long-term value, and whether the piece you're bringing home will still serve your family well years from now.

Your Guide to Furniture Payments in Central Florida

A family moves into a new home near Longwood. They need a sofa for the living room, a bedroom set for the primary suite, and maybe a dining table before the holidays. They walk through a showroom, sit on a few different styles, compare fabrics, and land on something that feels like home.

Then the conversation shifts from style to math.

That's where people often get stuck. They may know what they want, but they're not always sure whether to use cash, a credit card, a short-term installment plan, or store financing. They may also wonder whether it makes more sense to buy one room at a time or furnish more of the home now and spread the cost over time.

We've been helping Central Florida homeowners think through those choices since 1980, and the confusion is understandable. Furniture buying often happens during expensive life changes. A move, a renovation, a new baby, or a downsizing decision can all put pressure on the budget at the same time.

Why payment choices matter so much

Furniture is different from many everyday purchases because you're often solving several problems at once. You're trying to get the right scale, the right comfort, the right materials, and a payment structure that won't become stressful after delivery day.

A good payment plan should support a good furniture decision, not push you into a bad one.

That's why it helps to think beyond the tag price alone. Timing, order type, and product lifespan all matter. A custom American Leather sleeper or a solid wood Simply Amish dining set may deserve a different decision process than a quick fill-in piece for a guest room.

If you're shopping carefully, it also helps to understand the best time to buy furniture so your payment decision and purchase timing work together.

Comparing Your Main Furniture Payment Options

Not every payment method fits every household. The best choice depends on your budget, your timeline, and whether you value the lowest total cost, more short-term flexibility, or a predictable monthly amount.

The popularity of installment payments has climbed quickly. The Consumer Financial Protection Bureau reported that the number of BNPL loans originated in the U.S. by five surveyed lenders grew by 970% from 2019 to 2021 (CFPB BNPL market report). That doesn't mean BNPL is automatically the right choice. It means you're likely to see it often.

Furniture payment methods at a glance

| Payment Method | Best For | Key Consideration |

|---|---|---|

| Cash or Debit | Shoppers who want the simplest transaction and no ongoing balance | Ties up money you may need for moving, delivery, or other home costs |

| Credit Card | Buyers who can pay quickly or want card rewards and purchase protections | Interest can add up if the balance isn't paid off promptly |

| In-Store Financing | Larger purchases and planned monthly budgeting | You need to read the terms carefully, especially promotional language |

| Third-Party BNPL | Shorter installment plans and online-style checkout convenience | Missed payments or account stacking can create problems |

| Layaway | Shoppers who don't want to use credit and can wait before taking delivery | You usually won't receive the item until payments are completed |

| Rent-to-Own or Lease-to-Own | Buyers who need flexible approval paths | Total paid can be much higher than the original cash price |

Cash and debit

This is the most straightforward route. You pay, the balance is done, and you don't have to track a future bill.

For many households in Orlando, Lake Mary, and Sanford, the main advantage is peace of mind. There's no financing agreement to manage and no concern about interest. The tradeoff is liquidity. If you're also paying for movers, paint, appliances, or closing costs, using cash for furniture can leave you feeling squeezed.

Credit cards

Credit cards can work well when you already have a plan to pay the balance down quickly. Some shoppers also prefer the convenience, especially for a single purchase like a mattress, recliner, or accent chest.

The risk is simple. If the card balance sits for too long, the final cost rises. That's one reason many shoppers start asking whether a furniture-specific financing option might be easier to manage.

In-store financing

Store financing often makes sense when you're furnishing more than one room or investing in better materials that are meant to last. You get a structured payment plan, and that can make a larger purchase feel more organized.

If you're looking at craftsmanship-heavy pieces and wondering why some products cost more upfront, this guide on why furniture is expensive can help connect price to build quality, materials, and longevity.

Practical rule: Don't judge financing by the monthly payment alone. Judge it by the full amount you'll pay and the quality of the furniture you'll own at the end.

Third-party BNPL

BNPL providers appeal to shoppers who want speed and a familiar checkout flow. They can be useful for shorter repayment windows, especially when the purchase amount is modest compared with a full-house furnishing project.

Still, it's smart to understand how these products can fit into your broader credit picture. This overview of BNPL's effect on loan eligibility offers a helpful consumer-facing explanation of why multiple short-term obligations can matter when you're applying for other financing.

Layaway

Layaway is the quiet, old-school option that still works for some buyers. You reserve the item, make payments over time, and usually take it home after you've finished paying.

This can be a calm approach if you're disciplined and not in a rush. It's less useful if you need the furniture immediately.

Rent-to-own and lease-to-own

These programs are often marketed around approval ease and low weekly payments. That can be appealing when credit options are limited.

But shoppers need to be especially careful. Low weekly numbers can distract from the total cost over time.

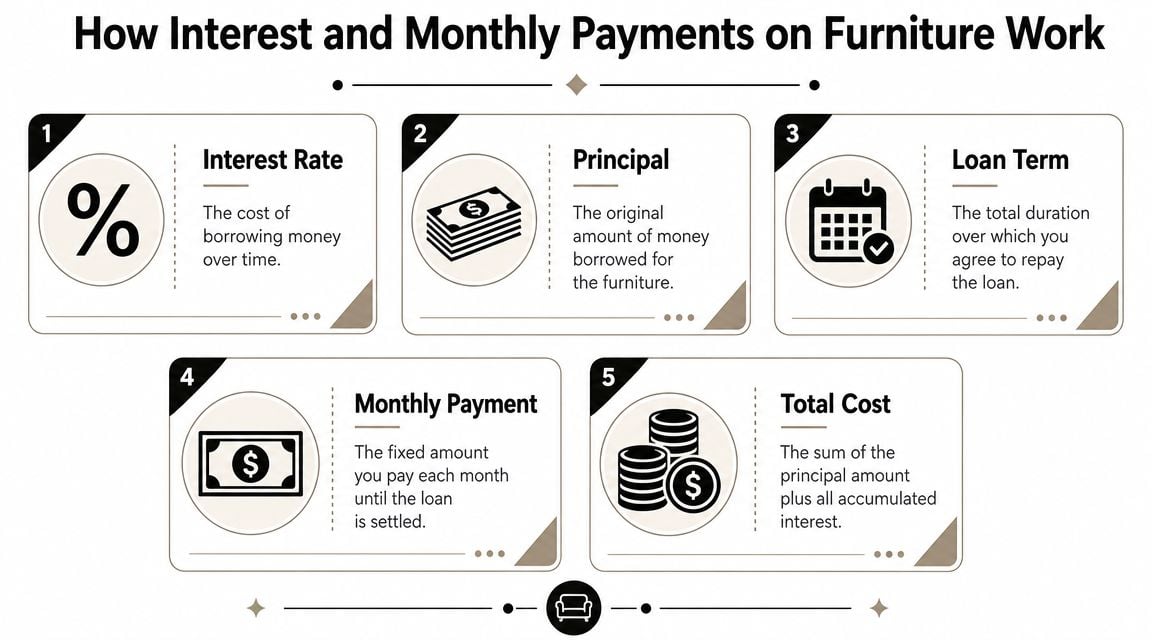

How Interest and Monthly Payments on Furniture Work

Most financing confusion comes from vocabulary. People hear terms like APR, promotional financing, and deferred interest, but the actual decision gets clearer once each term is translated into plain language.

Think of furniture financing like filling a cart in two parts. One part is the furniture itself. That's the principal, or the amount you're borrowing. The second part is the cost of borrowing that money over time. That's the interest.

The terms that matter most

APR means annual percentage rate. It's a way of expressing the borrowing cost over a year.

Loan term means how long you have to repay. A longer term often lowers the monthly payment, but it can also increase the total amount paid if interest applies.

Promotional financing often means a temporary special offer. Sometimes that means no interest if the balance is paid within a certain period. Other times, it may involve deferred interest terms, where interest can be charged if the balance isn't cleared as required.

A simple example

Let's say you're buying a Bassett living room set and financing part of the purchase. The exact monthly number depends on the agreement, but the process usually follows the same logic:

- Start with the purchase amount.

- Subtract any down payment you make.

- Review the APR or promotional terms.

- Check the loan term, such as the number of months.

- Confirm the monthly payment and the total amount paid by the end.

Here's where shoppers in Longwood often get tripped up. A lower monthly payment can feel safer, but if it stretches the loan much longer, it may not be the lower-cost choice overall.

If the paperwork is hard to explain in one or two clear sentences, pause and ask more questions before signing.

Why custom orders make payment planning important

Furniture purchases don't always happen in one simple transaction. A custom sectional, special-order dining set, or made-to-order recliner can involve deposits, later balance collection, delivery scheduling, and occasional adjustments if the order changes.

That's one reason payment systems matter on the retail side too. For furniture stores, integrated tokenized processing allows a payment gateway to encrypt card data and store a token for later charges such as deposits, final balance billing, or refunds instead of retaining the original card number (secure integrated card processing for furniture retail). For customers, that generally supports a cleaner and more secure payment flow during long order cycles.

Key Questions to Ask Before You Finance Furniture

Before you sign anything, slow the conversation down and ask direct questions. That one habit protects more shoppers than any promotion ever will.

A big knowledge gap in this category is the true cost of pay-over-time plans. Retail financing pages often spotlight low weekly payments, but they may not make the total repayment amount easy to compare, especially with lease-to-own offers (consumer financing and leasing page example). If you only focus on the small payment number, you can miss the bigger financial picture.

Questions worth asking out loud

- What will I pay in total if I follow this agreement to the end?

- Is the offer interest-free or deferred-interest, and what happens if the balance remains after the promotional period?

- Are there fees for late payments, setup, or early payoff?

- Can I pay extra early without penalty?

- What happens if I miss a payment by a few days or a full billing cycle?

- Does this account report to credit bureaus, and if so, how?

These questions don't make you difficult. They make you careful.

Questions to ask yourself

Some of the most important answers have nothing to do with the contract. They have to do with your life.

Are you furnishing a whole home after a move? Are you replacing one worn-out sofa? Are you buying a temporary piece, or are you investing in something you expect to keep for years?

If your credit profile is still developing, it may help to review practical steps to build credit before taking on a new payment obligation. Better credit habits can expand your options and improve how comfortable future financing feels.

You can also sharpen your buying process with this guide on how to shop for furniture smartly, especially if you're comparing quality levels and payment choices at the same time.

The smartest furniture financing decision usually happens before the paperwork starts, not after.

Your Flexible Payment Options at Slone Brothers

For many Central Florida shoppers, their primary goal isn't just to split up a bill. It's to make room in the budget for furniture they want to live with for a long time.

That matters when you're considering an American Leather sleeper, a Mavin dining table, a Smith Brothers sofa, or a Stressless recliner. These aren't impulse purchases. They're comfort, function, and craftsmanship decisions that affect daily life.

When financing can support a better purchase

A flexible payment option can make sense when it helps you choose the right piece instead of settling for the quickest one. That may mean selecting the size that fits your room, the fabric that fits your household, or the construction quality that holds up to years of use.

For shoppers comparing options, Slone Brothers Furniture financing options outlines available payment and financing paths. In practical terms, that can help when you're furnishing multiple rooms, planning a custom order, or balancing home setup costs after a move.

Matching payment choices to the way people really shop

A local showroom provides an advantage. Payments on furniture aren't just a checkout topic. They're tied to layout planning, fabric choices, lead times, and how the furniture will function in your home.

A few common situations where financing can be useful:

- Custom orders: You may want the exact leather, finish, or configuration instead of taking the closest in-stock substitute.

- Whole-room projects: Living room, bedroom, and dining purchases often happen together after a move.

- Quality upgrades: Better suspension, better tailoring, and better materials can be worth it when the piece is meant to last.

- Commercial furnishings: Business owners often need a coordinated purchase plan for office or waiting-area spaces.

Payment security also matters

Furniture orders can involve deposits, phone calls, delivery scheduling, and final balance collection. That creates more payment touchpoints than many retail categories.

For stores that handle in-store, phone, delivery, or commercial orders, point-to-point encryption or similar end-to-end encrypted payment capture helps keep readable card data away from employee systems and internal networks. Guidance discussed by BT's cyber security team also highlights alternatives such as DTMF masking and pay-by-link for remote payments, which can reduce exposure when customers don't pay in person (BT guidance on secure payment capture approaches).

If you're planning a room update and want help aligning budget, scale, and style choices, our in-house design team can help you think through the purchase as a complete project rather than a rushed transaction.

Making the Right Investment for Your Home

The right payment plan isn't the one with the flashiest wording. It's the one that fits your household without pushing you into regret.

That's especially true in Central Florida, where many buyers are furnishing a new home, replacing pieces after years of use, or trying to create a space that feels settled and comfortable for the long term. In those moments, value matters more than speed. A well-made sofa, dining set, or recliner can serve your family for years if you buy carefully and finance responsibly.

A practical budget helps here. If you want a simple framework before you shop, this article on household budgeting can help you think through furniture costs alongside the rest of your home expenses. It's easier to choose a payment plan when you know what room you have in your monthly budget.

You should also keep lifespan in mind. A lower upfront payment doesn't always equal better value if the piece won't hold up. This guide on how long furniture should last can help you weigh purchase price against durability.

Good furniture buying is part design decision, part budget decision, and part patience.

When those three work together, payments on furniture become a tool, not a trap.

Ready to find the perfect piece for your home? Visit the Slone Brothers Furniture showroom in Longwood, FL and let our design experts help you get started!